SMALL CAP VALUE: PLAYING WITH CYCLES (PART 1)

Generating excess returns by playing with factors' long-term cycles.

While both factors (small & value) have underperformed large caps growth stocks since the 2008 crisis, as those 18 years have been the ones of tech & large firms (helped by the rise of index investing), small-cap-value stocks may now be at a turning point.

(VERY) LONG-TERM

Indeed, financial research has documented for years the outperformance of small-cap-value stocks relative to large-cap-growth ones as (pre-2010) small-cap-value averaged an annual return of +14.8% while large-cap-growth only achieved +9.3%.

At this point, the reader would have nonetheless spotted an issue with this reasoning: the base effect. Indeed, stopping the long-term return measure in 2010, after a decade of small-cap & value factors’ outperformance may be misleading.

SMALL CAPS

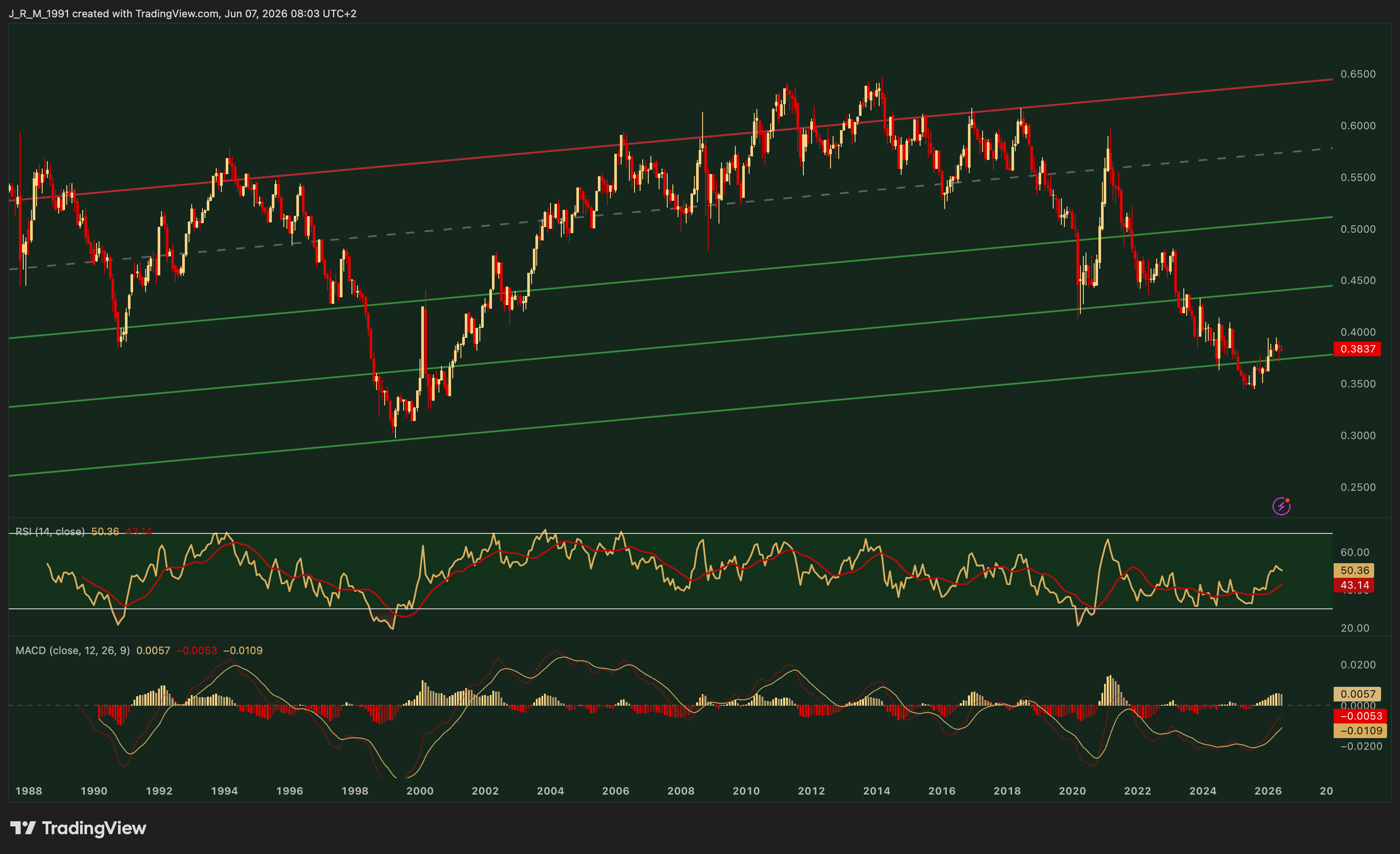

Nonetheless, the upward slopping trend of the Small-to-Large-Cap Ratio below suggests a long-term advantage in favor of small-caps, even if modest (+0.5% annual outperformance only).

Small-to-large-cap ratio ($SPX & $RUT used as proxies)

To this could be added a generally higher dividend yield, which also advocates in favor of small-caps.

While material, this outperformance isn’t, over the very long-term, drastic enough to justify a permanent overweight of small-caps.

PLAYING WITH CYCLES

However, as one may have noticed above, small-caps tend to follow (decade-long) periods of under- or outperformance relative to large ones.

This is the cyclicality investors could exploit in an attempt to generate excess returns.

Indeed, a simple statistical analysis allows one to identify that the ratio tends to:

• Top 1 standard deviation (σ) above its long-term trend (red line above).

• Bottom 3σ below trend (lower green line).

Investors having shifted from small to large caps as soon as the ratio was above +1σ, and from large to small caps as soon as -3σ were reached, would have generated the following excess (price) returns:

• 1987-1999 (long large caps): +87% relative to small caps

• 1999-2006 (long small caps): +97% relative to large caps

• 2006-2025 (long large caps): +64% relative to small caps

• 2025-today (long small caps): +6% over the past 15 months so far relative to large ones.

ENHANCED LONG-TERM RETURNS

We have seen here how “simply” playing with this factor could enhance investors’ long-term returns as it would have allowed, for 1987-2026 period, a massive 540% outperformance (or +4.8% annual excess return).

While this excess return is already impressive, we will see next weekend, in the second part of this paper, how other factors such as Value and Growth could be used as return enhancers, coupled with this size strategy.

Press the Subscribe button below not to miss my next publication.